The Return of Cocoa Volatility: Why the Market Just Shifted Again

- 15 hours ago

- 3 min read

For midstream processors, confectionery brands, and agribusiness stakeholders, the illusion of a stable cocoa market has officially shattered. Just as supply chains began adapting to the post‑2024 correction, July has delivered a sharp reversal. Intercontinental Exchange (ICE) futures surged overnight, catching the industry off guard and reigniting fears of prolonged volatility.

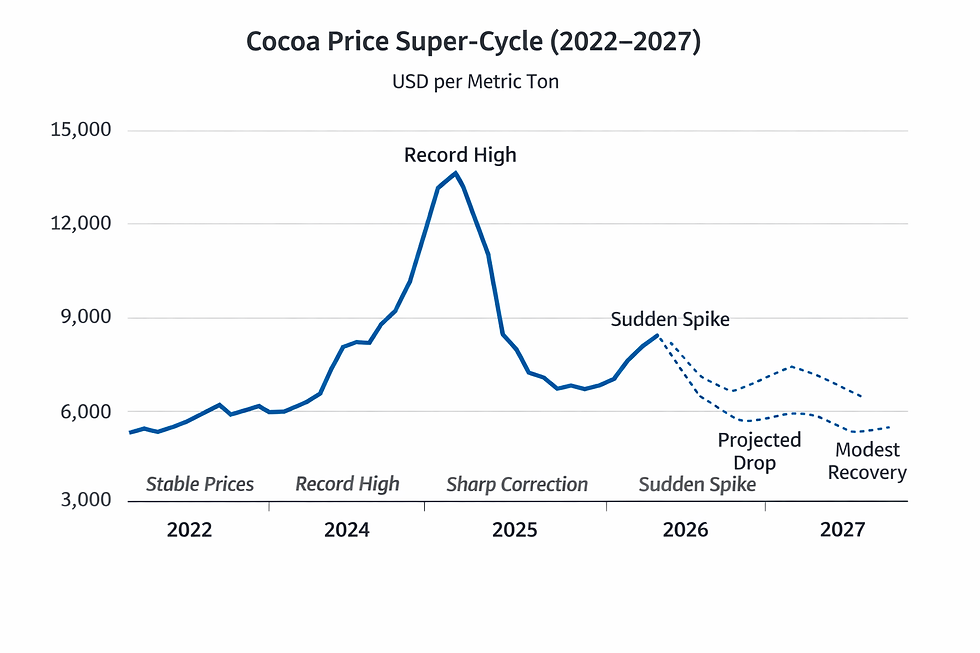

The so‑called “2026 reset” was short‑lived. After prices collapsed from their historic 2024 peak of nearly $12,900 per metric ton to a baseline of $3,000–$3,400, many believed equilibrium had returned. Yet the narrative has unraveled. Heavy rains in West Africa, looming El Niño risks, and liquidity constraints among smallholder farmers have converged to push prices higher once again.

Premium Cocoa Liquor / Cocoa Mass from Ghana (1MT)

$8,400.00$6,000.00

Buy Now

This is not merely speculation. The International Cocoa Organization projects a 478,000‑tonne deficit for the 2025/26 season; the largest in six decades. Meanwhile, compliance costs tied to the European Union’s Deforestation Regulation are reshaping midstream economics, far more than rumored tariff impacts. Together, these forces underscore cocoa’s structural fragility.

If your operational margins, procurement strategies, or portfolio valuations depend on the global confectionery supply chain, understanding the mechanics behind this latest pivot is no longer optional. Below is a high-level briefing on the structural forces reshaping the market today, and how you can access our comprehensive data breakdown.

The Illusion of the "2026 Reset"

Following the historic crisis of 2024; which saw cocoa prices scale an unprecedented peak near $12,900 per metric ton; the early months of this year offered a welcome reprieve. Aggressive demand destruction and destocking by global grinders successfully forced a sharp correction, pulling prices back down to a foundational baseline of $3,000–$3,400 per ton.

However, the narrative of a return to market equilibrium has collapsed. Over the last few weeks, the market has abruptly reversed, driven by a fresh wave of risk pricing in West Africa.

Shifting Fundamentals: Beyond the Headline Noise

To successfully navigate this pivot, professionals must separate speculative headlines from hard agronomic and macroeconomic data. The current price spike is being driven by three distinct, forward-looking catalysts:

The El Niño Threat: While recent heavy off-season rains have created immediate logistics bottlenecks and black pod disease risks, the primary driver for the upcoming 2026/27 main crop is the high probability of a severe El Niño pattern. Traders are aggressively hedging against projected moisture deficits in the West African cocoa belt.

The Liquidity Squeeze on Production: Reactive farmgate price adjustments by West African marketing boards earlier this year have heavily restricted smallholder liquidity. Farmers are facing a critical cash crunch precisely when capital is needed for essential chemical and fertilizer treatments.

Regulatory Overheads vs. Tariff Myths: Contrary to widespread rumors, raw cocoa import tariffs are not driving current cost pressures. Instead, the midstream sector is grappling with the tangible compliance costs of strict new supply-chain mandates, such as the European Union Deforestation Regulation (EUDR).

Anticipating the Next Capital Cycle

What does this mean for corporate procurement, hedging strategies, and retail pricing through the remainder of the year?

While institutional forecasts like the World Bank’s Commodity Markets Outlook project long-term normalization, the immediate horizon promises acute, localized volatility that will test the resilience of even the most diversified supply chains.

OTI's Head of Business Development commented on the current market situation:

Cocoa’s journey from stability in 2022 to historic highs in 2024, correction in 2025, and renewed volatility in 2026 illustrates the structural fragility of the market. Concentrated supply in West Africa, climate risks, and trade tensions ensure that cocoa will remain one of the most unpredictable commodities. While the World Bank projects a steep correction ahead, the current surge is a reminder that cocoa prices are shaped as much by weather and policy as by economics. For producers and processors, the task is to prepare for both extremes; the windfall of high prices and the strain of sudden declines.

Shea Olein - Biofuel and Food Grade (1MT)

From$1,586.00$1,550.00

Buy Now

Get the Complete Analysis

We have compiled a rigorous, data-driven market intelligence report designed for industry professionals who need to quantify these shifts.

Our full report, "Cocoa Prices Surge Again: Understanding the Market Dynamics," provides an exhaustive look into the sector's metrics, including:

A precise statistical timeline of the cocoa price super-cycle (2022–2026).

An audit of ICCO supply-demand balances and upcoming crop-year deficits.

Granular 2026–2027 price projections mapped against proprietary commercial desk consensus.

Strategic risk-mitigation frameworks for processors and CPG brands facing prolonged input inflation.

Don't base your Q3 and Q4 strategies on speculative news. Click here to read the full, data-backed market research report.

Comments